Joy to the World (Whether You Asked for It or Not)

European ecommerce order that just got redrawn

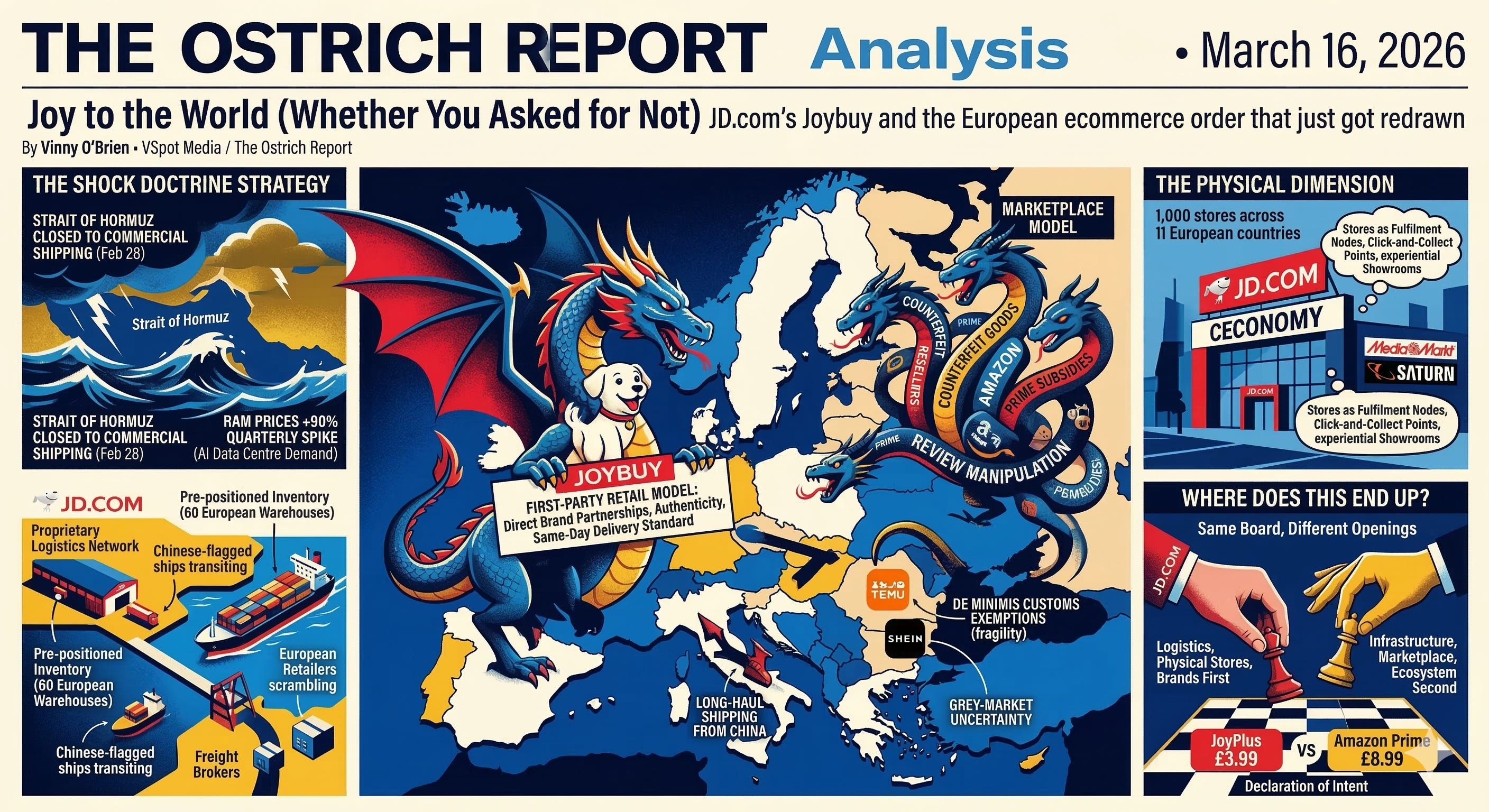

There is a scene near the beginning of Naomi Klein’s The Shock Doctrine where she describes the playbook used by those who understand that crisis is not an obstacle to ambition, it is the precondition for it. While the ground is still shaking, the prepared move. The unprepared scramble. The gap between those two states is where history gets written.

On …